Photo by Mateusz Dach on Pexels

Rising Concerns: The Growing Challenge of Retirement Savings

The story of a 60-year-old waiter with a mere $2,000 in a Roth IRA is not just a singular tale of financial anxiety; it is emblematic of a broader trend affecting millions of aging workers across the United States. As the cost of living continues to rise, particularly in urban centers, many older Americans find themselves inadequately prepared for retirement. The Economic Policy Institute reports that nearly half of households aged 55 and older have no retirement savings at all. This staggering statistic underscores a looming crisis that could strain social safety nets and alter the fabric of the American workforce.

While Social Security provides a safety net, it is often insufficient to cover basic living expenses. According to the Social Security Administration, the average monthly benefit for retired workers was about $1,800 in 2026. For those with minimal savings and increasing life expectancy, the prospect of relying solely on Social Security is daunting. The reality is stark: an increasing number of older workers anticipate extending their working years indefinitely.

Key Stakeholders: Perspectives and Pressures

The retirement savings crisis impacts a range of stakeholders, each with distinct perspectives and vested interests. For workers like our 60-year-old waiter, the immediate concern is survival. The fear of financial insecurity forces many to continue working in physically demanding jobs well past traditional retirement age. This raises questions about the quality of life and the potential health implications of delaying retirement.

Employers, too, face challenges as they grapple with an aging workforce. While seasoned employees bring experience and reliability, they may also require accommodations for age-related physical limitations. Moreover, the potential for increased healthcare costs is a significant consideration for businesses managing an older staff demographic. Employers must balance these factors while ensuring productivity and maintaining morale among a diverse age group.

On the policy front, government agencies are under pressure to address the shortfalls in retirement preparedness. Legislative measures aimed at incentivizing savings, such as tax-advantaged accounts, have had limited reach, with many low-income workers unable to contribute enough to make a meaningful difference. This gap indicates a need for more robust policy interventions to encourage savings and provide security for future retirees.

Economic Context: The Impact of Inflation and Wage Stagnation

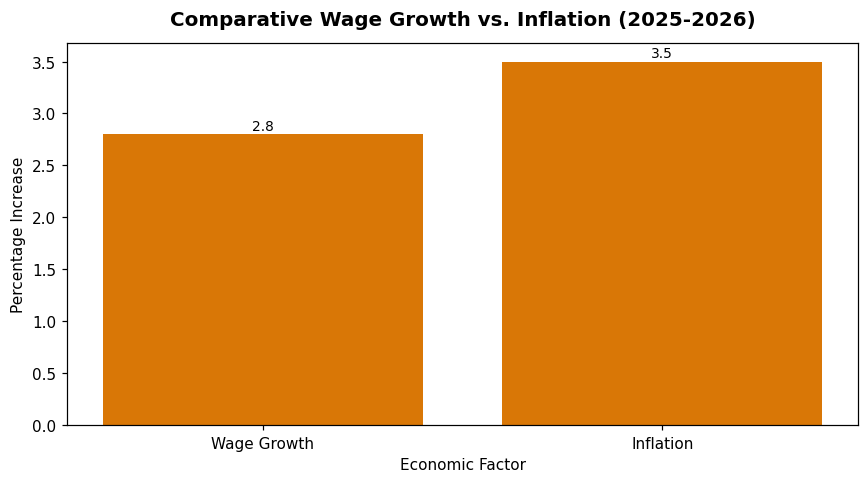

The broader economic landscape further complicates the issue of retirement savings. Inflation has outpaced wage growth for several years, eroding the purchasing power of workers across income brackets. According to the Bureau of Labor Statistics, the Consumer Price Index rose by 3.5% in the past year alone, while average hourly earnings increased by only 2.8%. This disparity makes it challenging for workers to allocate funds toward savings without compromising on immediate needs.

Moreover, the gig economy, characterized by short-term contracts and freelance work, has grown substantially. While it offers flexibility, it often lacks the benefits and stability associated with traditional employment, including employer-sponsored retirement plans. For many in the gig workforce, saving for retirement becomes an individual responsibility, often leading to inadequate preparation.

Real-Life Consequences: The Human Impact of Insufficient Savings

The concrete effects of insufficient retirement savings extend beyond financial hardship. For many older workers, the inability to retire means prolonged exposure to job-related stress and physical demands. The health implications are significant, with studies linking extended work in labor-intensive roles to higher rates of chronic illnesses and decreased life expectancy.

Beyond health, the societal implications are profound. As more individuals remain in the workforce longer, younger generations may face increased competition for jobs. This dynamic can exacerbate existing generational tensions and impact career progression for younger workers. Furthermore, the reliance on older workers to fill positions can slow innovation and adaptability within industries traditionally driven by youthful energy and new perspectives.

Looking Ahead: Policy Solutions and Market Adaptations

Analysts are closely monitoring the evolving landscape of retirement savings and its implications for both labor markets and social policy. Some propose expanding access to retirement savings plans through automatic enrollment in employer-sponsored plans or enhancing public pension systems. Others advocate for financial literacy programs that equip workers with the skills needed to manage their finances effectively throughout their careers.

Market adaptations are also underway, with financial institutions offering products tailored to the needs of older workers. These include annuities and other investment vehicles designed to provide steady income streams in retirement. However, the success of such products depends on widespread adoption and understanding among potential users.

As the nation grapples with these challenges, the role of innovation and policy reform becomes increasingly critical. Addressing the retirement savings crisis will require a concerted effort from government, employers, and individuals alike. The path forward lies in creating a more inclusive and equitable financial system that supports all workers in achieving a secure retirement.

Editorial Note: This article was produced with AI assistance and reviewed by the Celloraa editorial team for accuracy and clarity. It is intended for informational purposes only.

Read our Editorial Policy.

Leave a Reply